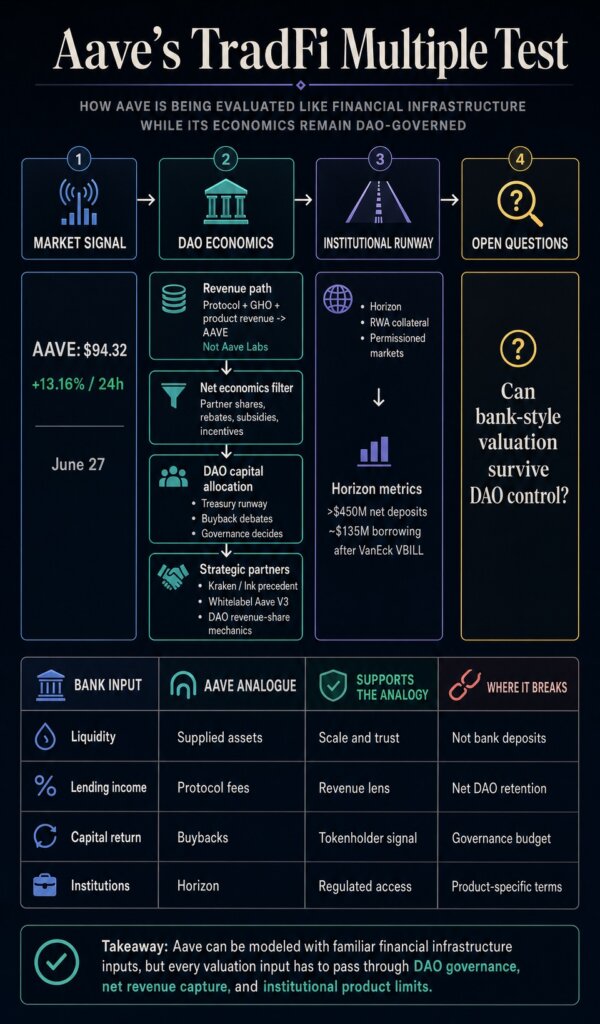

Aave’s latest market move is becoming a referendum on how investors value DeFi lending as its economics begin to resemble those of financial infrastructure.

The token rallied as AAVE traded around $94.32 on June 27, up 13.16% over 24 hours. At the same time, a reported Standard Chartered bull case described Aave in automated-bank terms, while reports of Kraken parent Payward discussing a strategic stake in an Aave-related entity put fresh attention on the line between Aave Labs and AAVE-aligned protocol economics.

Stani Kulechov moved that line to the center by saying Aave protocol, GHO, and product revenue flow to AAVE rather than Aave Labs. The practical question is how that revenue reaches the Aave DAO after partner shares, incentives, governance decisions, and product-specific arrangements.

Aave is being tested as a DAO-owned financial infrastructure that can capture net revenue, allocate capital, and reach institutional markets while keeping core economics outside a conventional company balance sheet.

Why investors are reaching for bank-style math

Aave already has a scale that outside capital can recognize. The Aave protocol dashboard tracks the lending market’s locked value and activity, while AAVE ranks among the leading lending and borrowing assets by market value.

Those figures explain why bank-style language has entered the discussion, even though they require careful translation before they become tokenholder economics.

Traditional lenders are valued through inputs that investors know well: liquidity, borrower demand, fee capture, risk management, and capital return. Aave has crypto-native versions of those inputs.

It has supplied liquidity instead of bank deposits, smart-contract markets instead of loan officers, governance instead of a board, and tokenholder-aligned buyback debates instead of corporate capital-return policy.

The comparison is useful, yet every input has a structural caveat. The protocol scale is visible, but suppliers are users of smart-contract markets rather than bank depositors.

Fees and product activity can grow, but gross protocol activity differs from the net revenue retained by the DAO. Buybacks can create a clearer capital-allocation lens, but the budget and execution depend on public governance rather than corporate management.

Aave’s current valuation debate sits inside that gap. The market is trying to decide whether open lending infrastructure can be underwritten with familiar financial tools while the governance and revenue rights remain token-native.

The Aave Will Win framework gives that debate a concrete mechanism. A governance temp check and later ARFC discussion describe Aave-branded product revenue as flowing to the DAO.

The same framework defines revenue after external partner shares, rebates, subsidies, and user incentives, which keeps the cash-flow case tied to net economics rather than headline activity.

Aave’s DAO funding discussion adds the capital-allocation layer. Buybacks give investors a familiar signal, but the relevant decision-making sits in treasury runway, governance appetite, and contributor priorities.

That structure is central to Aave’s difference: the protocol can adopt financial-company tools while keeping the levers in DAO hands.

Bank-style inputAave analogueWhy it supports the analogyWhere the analogy breaksDeposits and liquiditySupplied assets across lending marketsShows scale and user trustSuppliers use smart-contract markets rather than bank accountsLending incomeProtocol fees, GHO, and product revenueGives investors a revenue lensGross activity differs from DAO-retained net revenueCapital returnDAO-governed buybacksCreates a clearer tokenholder economics storyBudgets and execution depend on governanceInstitutional productsHorizon and tokenized collateral marketsMakes Aave legible to regulated capitalCompliance, partner economics, and risk controls remain product-specific

Strategic interest sharpens the Labs-versus-protocol distinction

The reported talks between Kraken and Payward add pressure, suggesting centralized crypto firms may seek strategic exposure to Aave’s lending stack. The evidence supports reported talks around an Aave-related stake, while Kulechov’s clarification separates Aave Labs-related allocation or partnership interest from AAVE/DAO protocol and product revenue.

That distinction changes the market interpretation. If strategic interest is about an entity, allocation, or distribution relationship, the protocol economics still need to be traced through governance frameworks and DAO-controlled revenue paths.

Investors cannot simply treat AAVE as corporate equity in Aave Labs. They also cannot ignore the fact that commercial partners may help the protocol reach users, liquidity, and regulated distribution channels.

Aave already has a Kraken-related commercial precedent. A governance proposal for Ink, Kraken’s Ethereum layer 2, laid out a whitelabel Aave V3 instance with revenue-share mechanics for the DAO.

That record makes the latest strategic-interest discussion part of a broader commercial question: how much distribution, branding, and economics should the DAO share to expand the protocol’s reach?

Bank-style valuation is both attractive and fragile here. Predictable revenue, capital returns, and institutional channels can support a higher-quality multiple. Public governance, tokenholder rights, and partner economics can complicate the comparison.

Aave’s test is whether those pieces can stay coherent as more traditional capital tries to model the protocol.

That framing keeps the reported stakeholder discussion in proportion. It shows a path for strategic partners to plug into Aave’s distribution and product surface, while token economics still depend on governance-level decisions.

The more centralized partners appear around the protocol, the more valuable the Aave Labs/DAO distinction becomes. Investors looking for bank-style metrics have to follow the economics from product revenue to DAO treasury, then from treasury policy to buybacks or other allocations.

That route is slower than corporate earnings guidance, yet it preserves the protocol’s native structure.

Horizon turns the test toward institutions

Horizon makes the institutional side of the argument concrete. Horizon gives Aave a venue for real-world-asset collateral and permissioned institutional markets, and the VanEck VBILL update said Horizon had reached more than $450 million in net deposits and about $135 million in borrowing after adding the fund.

Those figures support the idea that Aave can become legible to regulated borrowers, asset managers, and tokenized-asset issuers. They also keep the valuation debate grounded.

Horizon is an institutional RWA product, rather than the whole Aave protocol, and its economics still need to be read through the lens of product design, partner terms, and DAO governance.

The next signal is governance quality as much as price. Institutional capital tends to reward familiar cash-flow structures, service expectations, and clarity of compliance.

Aave’s value proposition depends on making those rails useful while preserving DAO-controlled economics.

If governance keeps revenue capture, buybacks, and institutional partnerships coherent, Aave could become the clearest case for a DAO-owned financial network earning a traditional-finance multiple.

If that balance weakens, the bank analogy becomes a ceiling rather than validation, because the economics that make Aave distinct would become harder to price through the token.

Be the first to comment